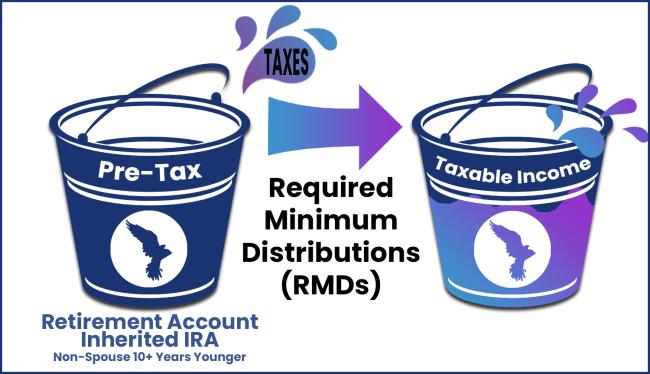

Required Minimum Distributions (RMD’s) – how they impact you AND your heirs | Tax Planning

The IRS is going to get paid on your pre-tax bucket (and maybe the state you live in). Maybe this year, maybe later, maybe after you are gone. When you turn 73 (unless you did prior to 2023), the IRS makes you withdraw funds from your pre-tax bucket. These withdrawals are called REQUIRED MINIMUM DISTRIBUTIONS (RMD’s) and are taxed 100% as ordinary income. If you are alive, they are based on your life expectancy and the account balance(s) at the end of the previous calendar year.

If you have done a great job of saving in your pre-tax bucket (Traditional IRA, 401(k), etc.), your RMD’s can be quite significant. For example, if your Traditional IRA balance on December 31, 2023 was $1 million and you turn 76 this year, your RMD would be $50,632.91 (source: https://www.investor.gov/financial-tools-calculators/calculators/required-minimum-distribution-calculator). If you live in Colorado and are in the 22% tax bracket, you would be looking at a potential tax bill of $13,367.

The other situation we run into is when pre-tax accounts get passed to non-spousal beneficiaries (your children). They are now put on a 10-year clock to withdraw 100% of the funds from the account and pay income taxes on it. Using the same $1 million Traditional IRA and 6% annual growth, the beneficiary would need to withdraw at least $29,891 each year to avoid penalties at the end of 10 years. Beneficiaries also LOSE the ability to convert this bucket to a tax-free bucket (an option that YOU have before you are gone and before your RMD’s start). They must take the RMD’s as ordinary income which could also hurt their ability to pursue several of the strategies that we have mentioned in previous emails (conversions, for example). The increase in taxable income could also trigger shadow taxes, if they are old enough to be on Medicare or taking Social Security.

We really believe that nobody wants to send a ticking tax bill bomb to their beneficiaries. You might still have to time to consider shifting funds into the tax-free bucket prior to starting your own RMD’s OR prior to your account(s) passing to your heirs. As always, we encourage the idea of doing SOMETHING, even if it’s small. Start working on paying the IRS now and get ahead of the pending tax bill that we all know is coming.

Next up: Qualified Charitable Distributions (QCD’s) – What are they and their tie to RMD’s

Disclosures

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

Information and interactive calculators are made available to you as self-help tools for your independent use and are not intended to provide investment, tax, or legal advice.

We cannot and do not guarantee their applicability or accuracy in regard to your individual circumstances. All examples are hypothetical and are for illustrative purposes. We encourage you to seek personalized advice from qualified professionals regarding all personal finance issues. (57-LPL)

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.